One of the biggest mistakes first-time campground buyers make is underestimating how much capital is actually needed to purchase and operate a campground successfully.

Buying the campground is only the beginning.

Operating it successfully is the real challenge.

Typical Financial Expectations

✔ Down payment: often 25–30% minimum

✔ Closing costs: typically 3–5%

✔ Working capital: often $30,000–$100,000+ depending on park size and operations

✔ First-year reserve or “surprise fund”: always recommended

These numbers can vary depending on:

- lender requirements

- campground size

- operational complexity

- occupancy structure

- financing type

- and overall risk profile

Working Capital Matters More Than Most Buyers Expect

Many buyers focus heavily on:

- the purchase price

- and the down payment

…but underestimate the amount of cash needed AFTER closing.

This is where many buyers get into trouble.

Campgrounds are operational businesses with constantly changing variables.

Things may have worked perfectly yesterday:

- but not today

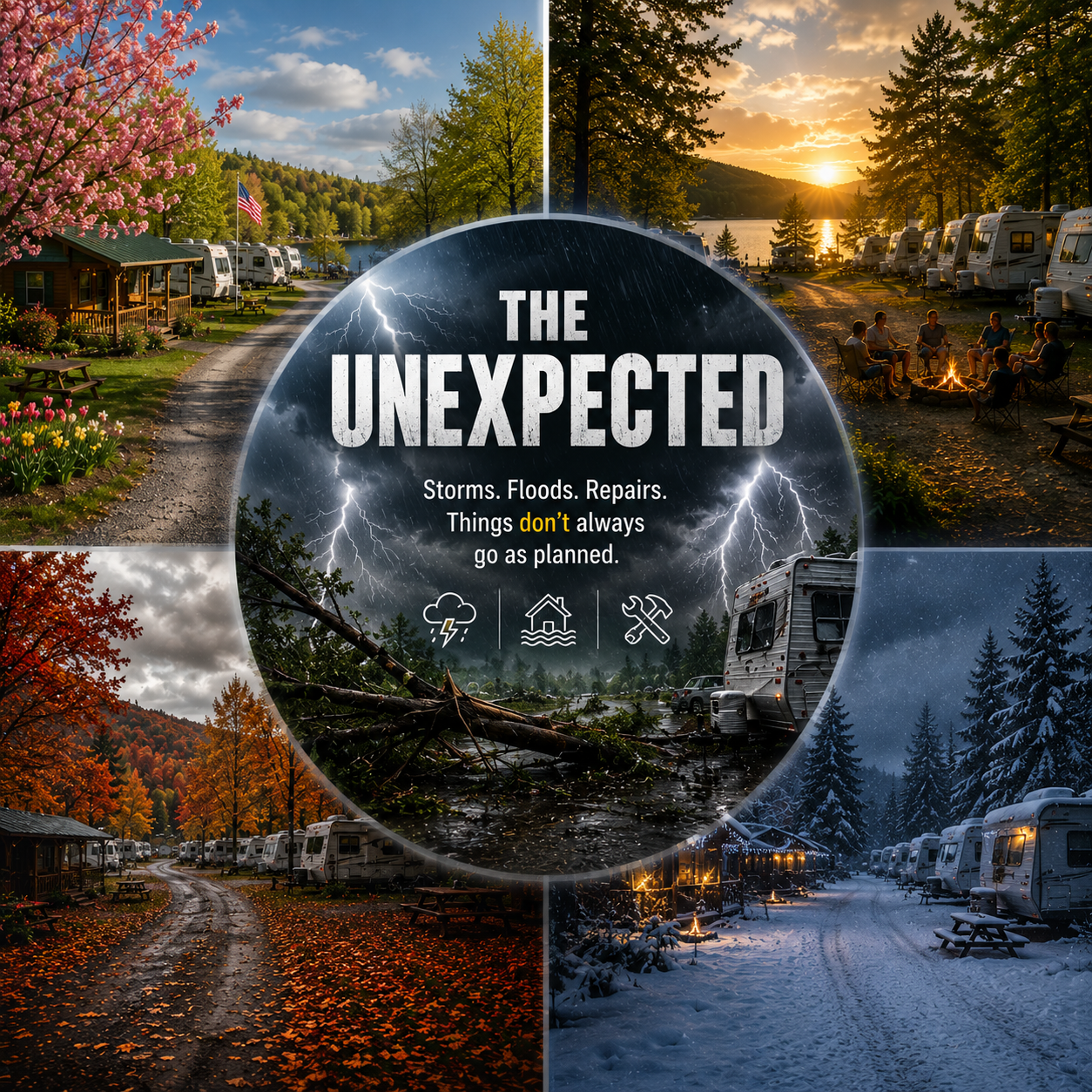

Unexpected situations happen constantly, including:

- unseasonal storms

- extreme heat

- heavy rain weekends

- wildfire smoke

- road closures

- utility failures

- equipment breakdowns

- staffing shortages

- excessive bugs or weather events

- slower tourism seasons

- or emergency repairs

Surprise costs are part of campground ownership.

Strong buyers prepare for them before they happen.

All of these situations eventually impact the business financially.

At the end of the season, these operational disruptions often show up directly on the campground’s P&L through:

- reduced occupancy

- lower revenue

- increased maintenance costs

- emergency repairs

- higher labor expenses

- refunds

- insurance claims

- utility increases

- or unexpected operational costs

This is one reason campground financial performance can fluctuate significantly from year to year.

Understanding that campground ownership requires planning not only for normal operations — but also for the unexpected.

Why Financial Cushion Is Critical

Without adequate reserve funds and working capital:

- small problems can become major financial stress quickly

A campground may still:

- need road repairs

- utility upgrades

- pump replacements

- mowing equipment

- insurance adjustments

- or unexpected maintenance

…even immediately after closing.

This is why experienced campground professionals strongly encourage buyers to maintain:

✔ financial breathing room

—not just enough money to barely close the deal.

Understanding Down Payments

Most traditional campground financing still requires meaningful buyer investment into the transaction.

Many lenders and sellers want to see buyers contribute approximately:

✔ 25–30% down or more

Why?

Because lenders want buyers to have:

- real financial commitment

- operational stability

- and financial cushion entering ownership

In many cases:

✔ borrowed down payments are not allowed by lenders.

Lenders generally want buyers to show:

- real liquidity

- reserve strength

- and financial stability

before approving campground financing.

Opportunity vs “Deals”

Many buyers entering the industry focus heavily on:

- lowering the purchase price

- negotiating reductions

- or trying to structure the smallest possible upfront investment

In many situations, these negotiations are driven more by:

- financing limitations

- lack of reserve capital

- or weak operational cushion

…than by the actual quality of the campground itself.

Experienced campground buyers understand that long-term success is often determined more by:

- operational strength

- financial preparation

- reserve capital

- and future opportunity

…than simply negotiating the lowest possible purchase price.

Strong campground ownership requires enough financial stability to:

- operate the business properly

- handle surprises

- reinvest into the property

- and support long-term growth

The goal is not simply:

“How little money can I put down?”

The better question is:

“Do I have enough financial stability to operate this campground successfully long term?”

Financial Preparation Creates Stability

Strong campground buyers prepare financially BEFORE purchasing.

This includes planning for:

- down payments

- closing costs

- reserve funds

- operational surprises

- seasonal fluctuations

- and future improvements

Campgrounds reward buyers who plan ahead financially.

Underestimating capital needs can create stress quickly, especially during the first few years of ownership.

LESSON TAKEAWAY

Buying a campground requires more than just enough money to close the transaction.

Strong campground ownership also requires:

- working capital

- reserve funds

- operational cushion

- and realistic financial planning

The buyers who succeed long term are usually the ones who prepare for:

the unexpected before it happens.

“The campground purchase is only the beginning — keeping the business financially healthy is what matters long term.”